Google Search Volume & Trends for the UK Car Insurance Market

“Car Insurance” Google Search Insights : Summary

Based on the findings below we discovered that:

Q1 of 2023 has seen the highest monthly peaks in demand indicating 2023 is going to be a record breaking year

4.5 Million historical searches in March 2023 was a new record

4M in Sept 2020 was the previous highest ever peak in demand

Current consumer demand for car insurance is approximately 4-6 million searches per month

Mid-Market Google Ads budgets range from £500,000 to £1,200,000 (per month)

Consumers are very brand savvy with the largest proportion of searches (45%) going to Brand terms

Admiral car insurance is the market leader

There is not much nuance to search terms which results in fierce competition for very generic terms

34% of searches were for general “car insurance” terms

the most searched for term by 2:1 was for people searching exactly for [car insurance]

What is the search volume for people looking to purchase car insurance?

This simple question is quite hard to answer as it is open to interpretation but we can provide answers within a specific framework for a range of scenarios. In this case we are focusing on Google search volume of specific keywords that signal intent to purchase or renew car insurance. For this study, we’ve defined hundreds of relevant search queries and excluded other terms that are ambiguous or irrelevant. Auditing this dataset from Google Ads own Keyword Planner tool will provide an estimation of the size of the car insurance industry in the UK, based on consumer search behaviour.

As this is pure search volume data from Google it is relevant for either SEO or PPC.

The consumer demand for car insurance is approximately 4-6 million searches per month

Historical Trends, which are analysed in more detail below, suggest 3.5 million - 4.5 million searches per month

Forecast Scenarios, which have slightly less exacting criteria but can pick up on recent trends estimates the range to be 4.5M - 6.5M searches per month

Historical and Forecast data are two separate data sets that provide different outputs from the same inputs. As such both should be analysed and both are correct, given their context. Comparing them can be tricky or possibly not even recommended so try and view them in isolation!

Competitive Analysis of the Car Insurance Industry

We have established that there are 4-6 million searches per month for car insurance related terms regardless of whether this is from an organic or paid search perspective.

The next step of the market analysis is to establish how competitive these terms are. We can estimate the paid search marketing budget required to capture some, most or all of the market share with Google’s keyword planner tool. The output can be used directly to support a business case for paid search. This budget will also provide a proxy for the difficulty in ranking for these terms organically or as a portion of the marketing effort (cost) required in a cross-channel marketing plan.

Estimated Ad spend per month as Market Share changes

The car insurance market is super competitive! To capture all of the demand and be near the top of the auction results would comfortably require monthly budgets of between £750k - £2 Million per month.

(Relatively) modest budget of £50k - £100k would still show an Ad to 1M+ searches.

Given that the dominating market share position (6.6M monthly searches) costs 5x the mid-market share position (of 3.3M searches per month) implies the competition is top heavy

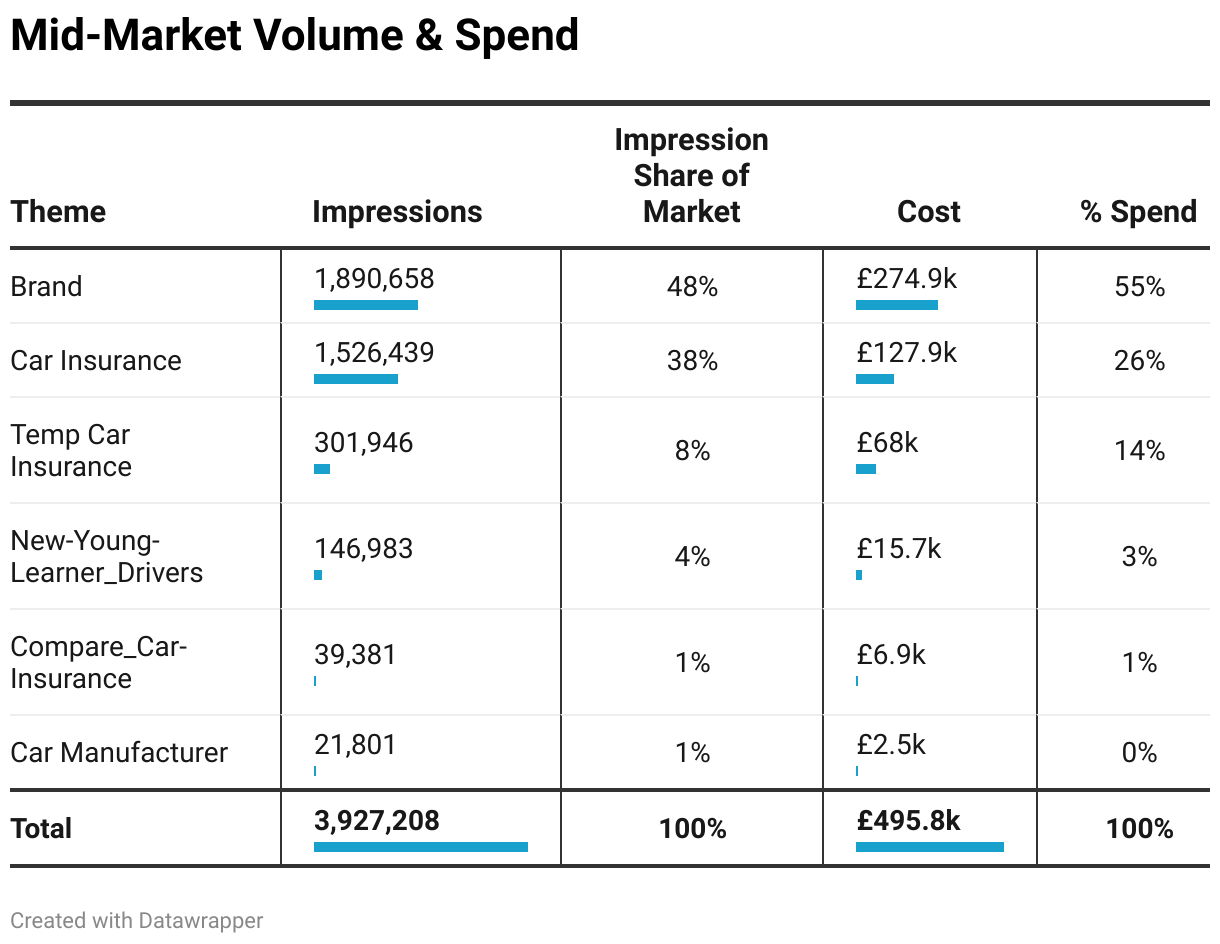

For the rest of this section we’ll look at mid-market forecast data by keyword and category to get a better feel for the space, using an advertising budget of £500k / month.

Where would the money go

Avoid or selectively bid on competitor brand terms e.g. those close competitors that compete head-to-head

With more that 50% of spend going in 50% of Brand search volume suggests budgets could be used more effectively on non-brand terms

Bid on generics as

General car insurance terms have enough volume if not much depth but are less competitive than other niche terms

Avoid Temporary Car Insurance terms unless that is your niche

As these are twice as competitive as any other theme (niche volume captures 8% of market but for 14% of budget)

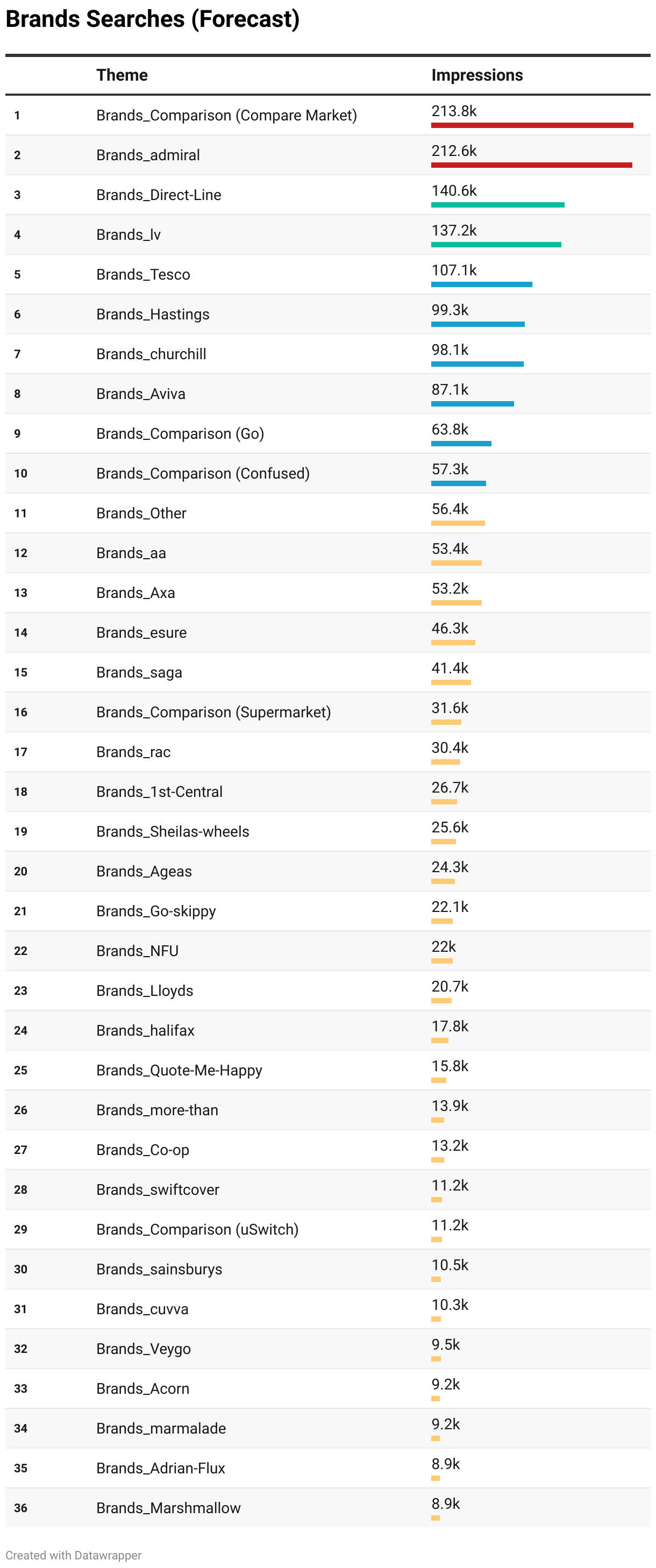

Demand for Brands!

Main searches by consumers are for the well known brands and comparison sites in the UK

Admiral competes head to head with Compare the Market both of which dominate

Direct Line and LV follow some way behind (with more detail on this in the historical trends section below)

Tesco, Hastings, Churchill and Aviva follow in the next trenche

The other well known “Comparison” sites make up the rest of the top 10 slots

More volume is revealed within the long-tail of brands than are picked up by the “historical” trends (later in this report)

Shiela’s Wheels, Quote Me Happy and further down Veygo, Marmalade & Marshmallow

Historical Search Trends for Car Insurance

Looking back at the Historical Data Set provides more insight and another opportunity to make robust decisions about the quality and trustworthiness of the data set provided by the “forecast”. Rather than relying on a snapshot of a single forecast month we can trend the market demand and changes in consumer behaviour over time going back many years.

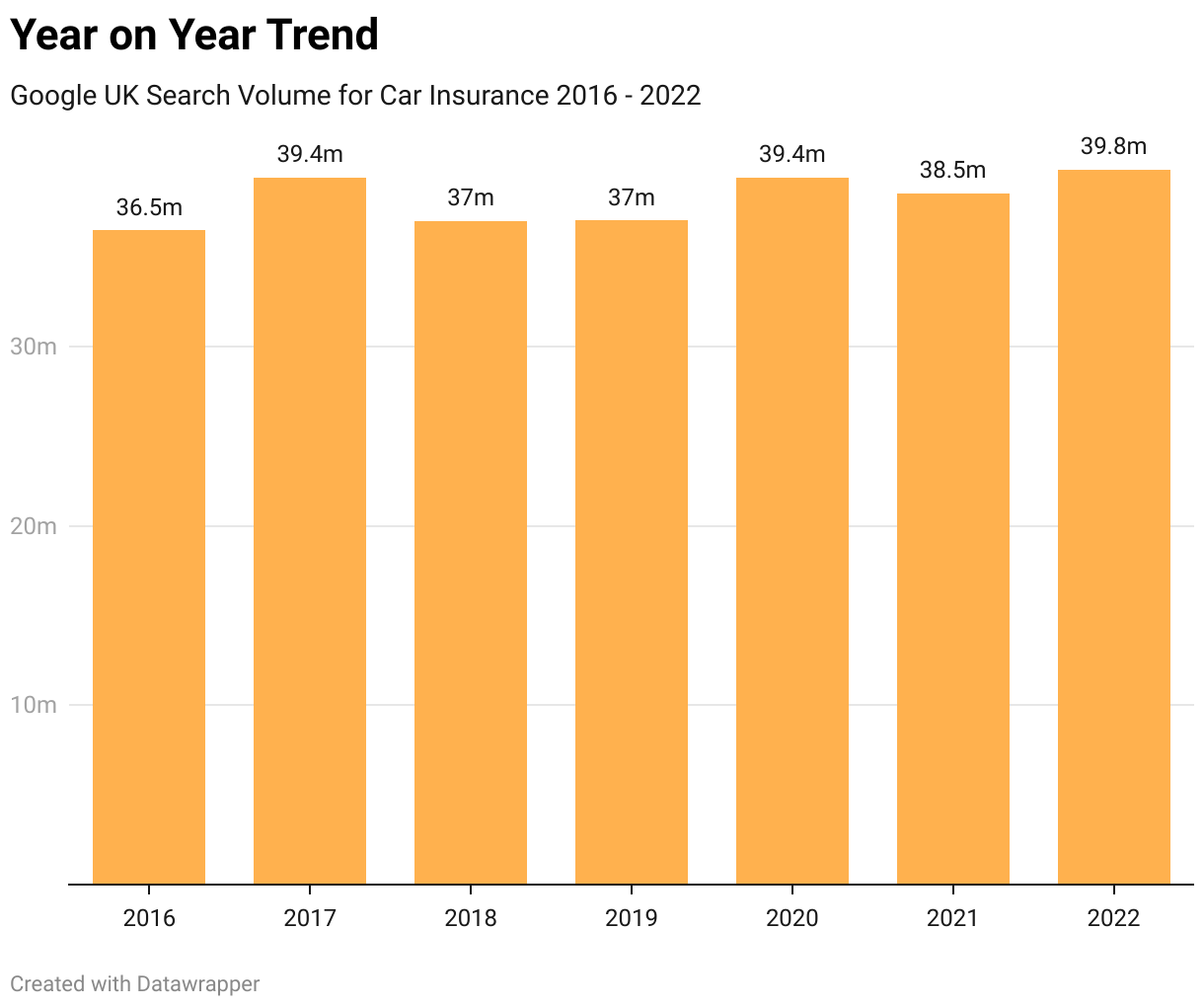

Yearly Trends

UK Covid restrictions in place between March 2020 - March 2022.

Google impression volume data shows that the car insurance market is incredibly robust and consistent.

Last full year 2022, was the highest it’s been since this study began

2020 - 2022 search volume was not diminished by Covid

Average of 38.5M searches per year between 2017 - 2022

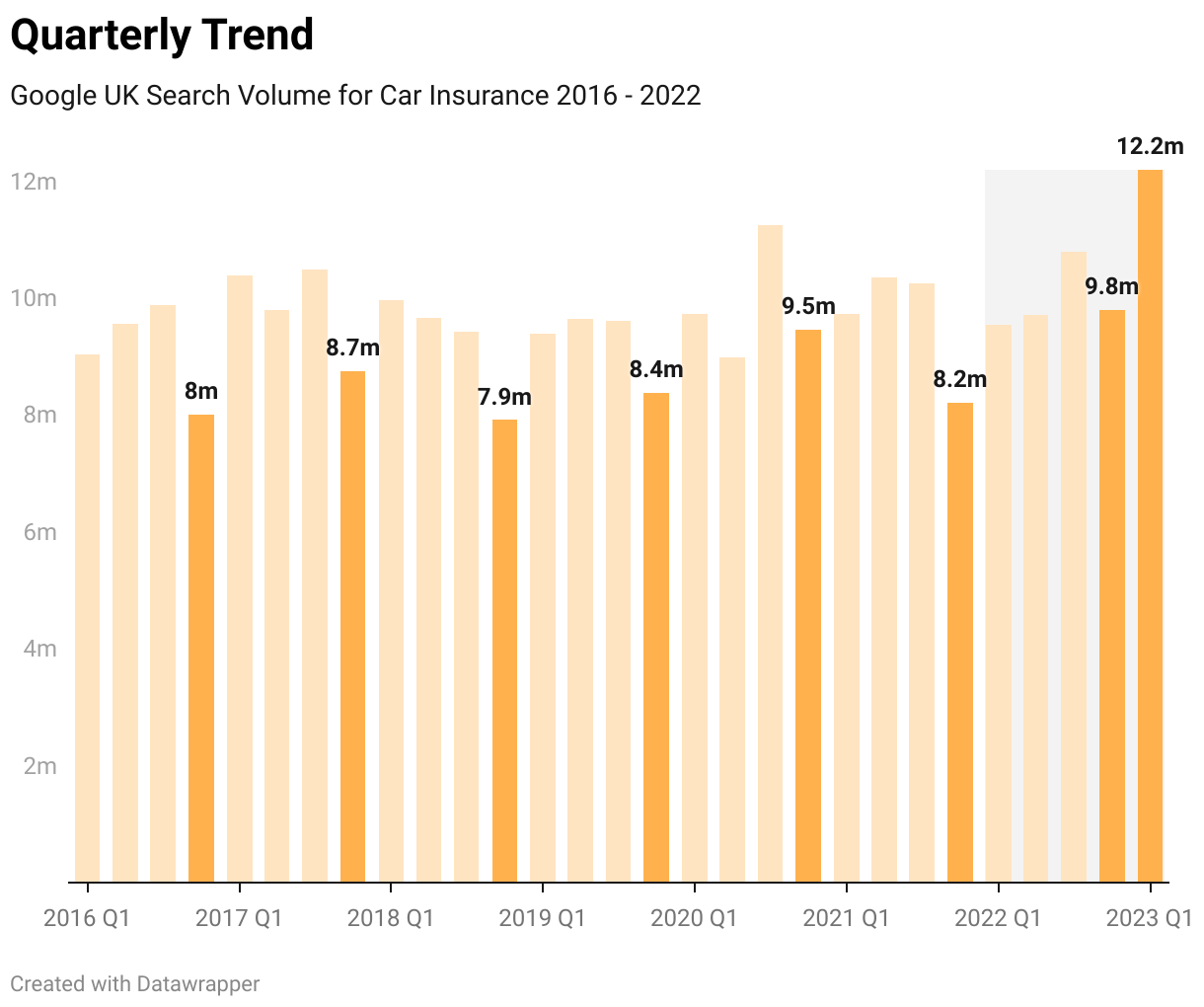

Quarterly Trends

Q1 of 2023 (which is all the data I have at this time) shows record levels of demand

The shaded area shows consistent quarterly growth indicating 2023 is set to be a record year

2022 Shows stepped increase in Q1-Q4 demand per quarter, with Q4 also being a “relative” peak for that quarter compared to the average

Demand across Q1 > Q2 > Q3 is either consistent and flat or there is gradual step increase from Q1 to Q3

Unsurprisingly Q4 is when the lowest demand occurs and this is consistent year on year

Monthly Trends

Jan, Feb and March 2023 show record demand are among some of the highest peaks recorded

March 2023 is the highest demand seen reaching 4.5 Million searches. The previous peak was Sept 2020 which had 4 Million searches

There has been overall growth over the recent years with:

3.2M in 2019

2020 had lockdown lows and surges to make the difference

The second half of 2022 saw a rise in demand to 3.5M which lasted from the summer and longer into the autumn month, with Nov and Dec recording 0.5M more searches per month than usual

Google Trends

In isolation to the current data set another source to lean on is of course Google Trends. The graph below shows weekly volumes (indexed) so it is not directly comparable with the keyword planners monthly perspective (but it’s still a useful data set).

If the graph does not appear or does not look accurate then you can see it directly on google trends here.

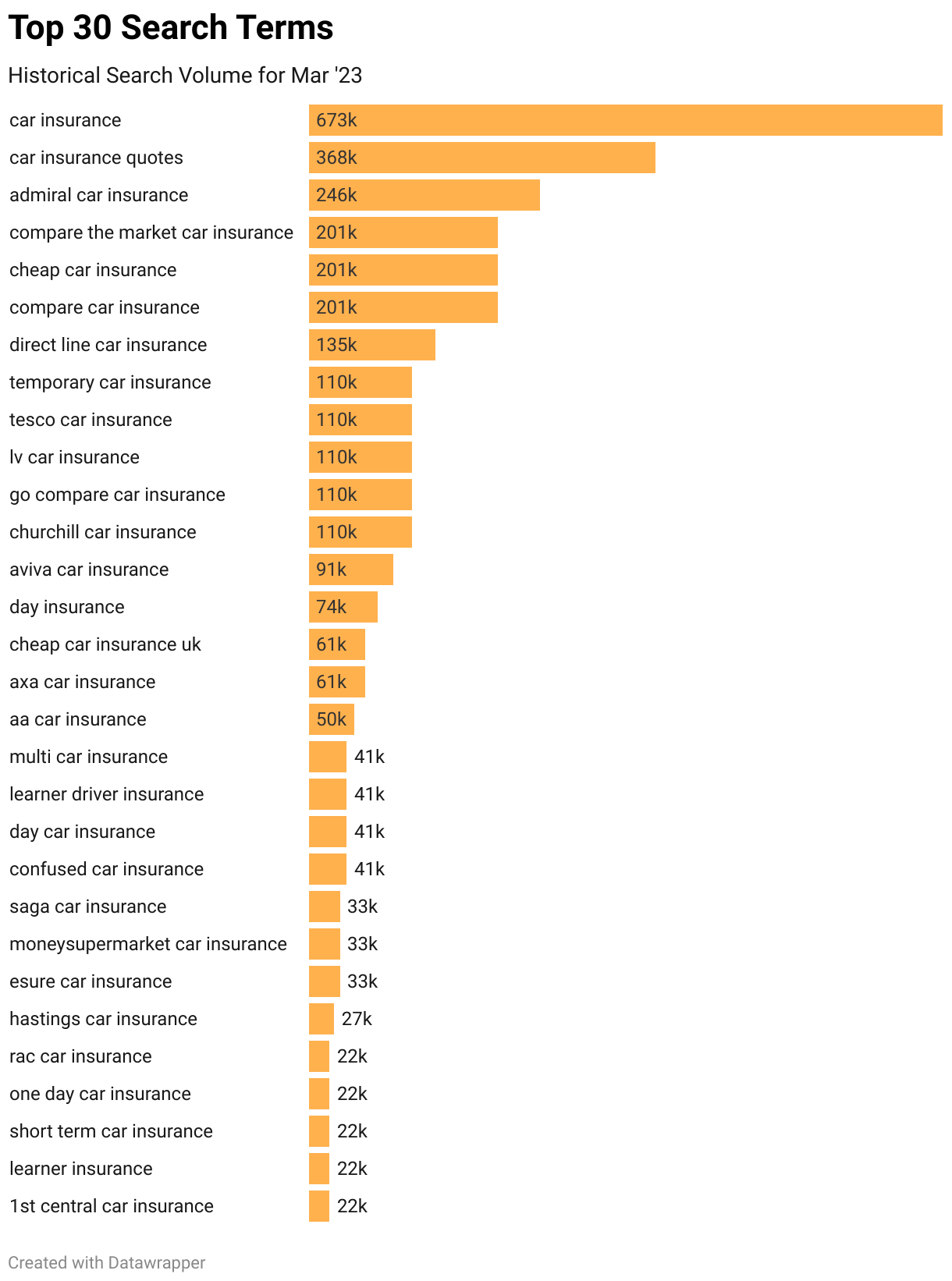

What are People Searching For When It Comes To “Car Insurance”?

When people are searching for car insurance, the most popular query by far is a search for, you guessed it, ‘car insurance’ and ‘car insurance quotes’!

Other themes are a bit more surprising however:

“Admiral car insurance” is the next most searched for term before any other generic or any other brand or comparison site

Temporal terms show high on the list such as ‘temporary car insurance’ and ‘day insurance’

Almost half of the search volume is for specific insurance brands e.g. “direct line”, “admiral” or “compare the market car insurance”

Users don’t get very specific when it comes to the make of car they want to insurance

Searches for insurance by specific car manufacturers (e.g. “bmw car insurance”) is insignificant

“time related” searches e.g. “temp car insurance”, “one day car insurance” account for 12% of the total search volume but most of this is focused on a handful of terms, making them more competitive than any other theme

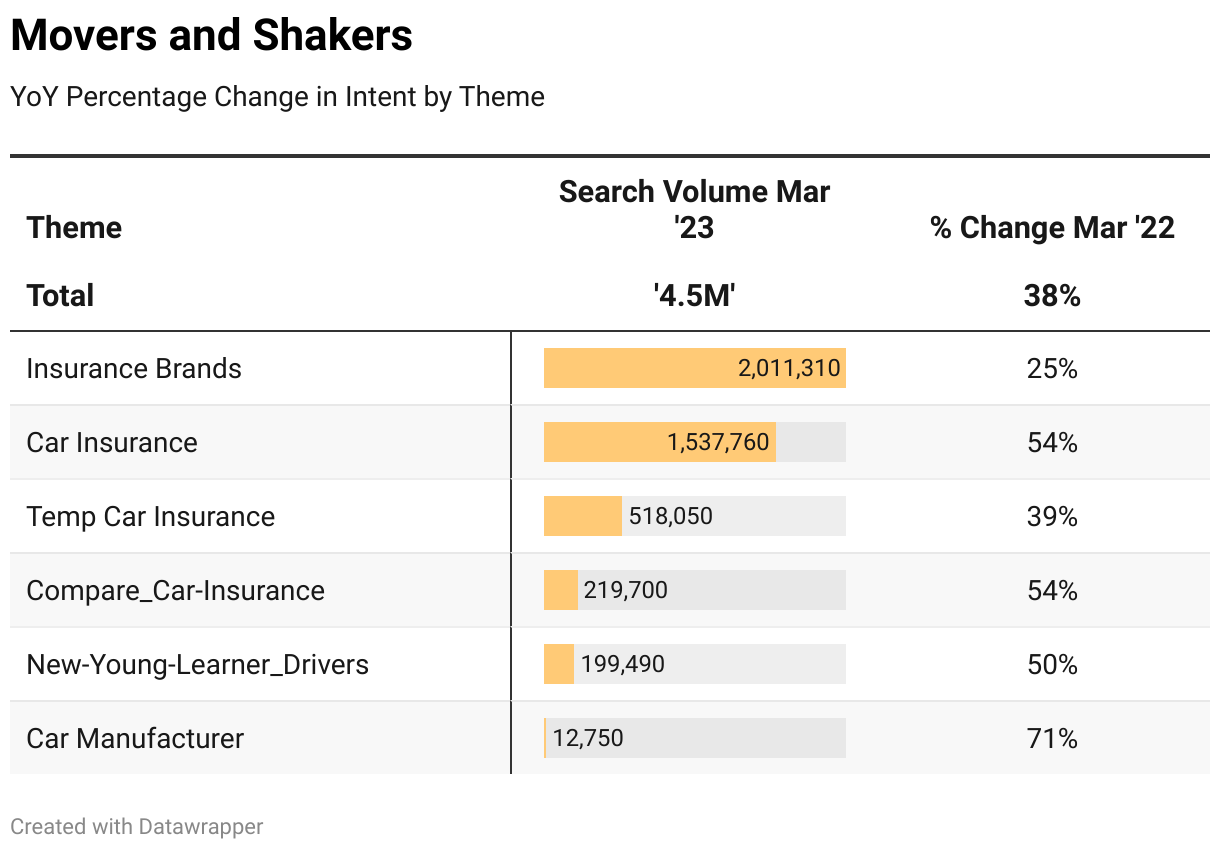

March 2023 search volume was up 38% overall compared to this time the previous year

All Themes saw a rise in demand

Generic “car insurance” volumes increased significantly

Other niche car insurance terms grew more than the Insurance Brands which may offer some hope to smaller market players

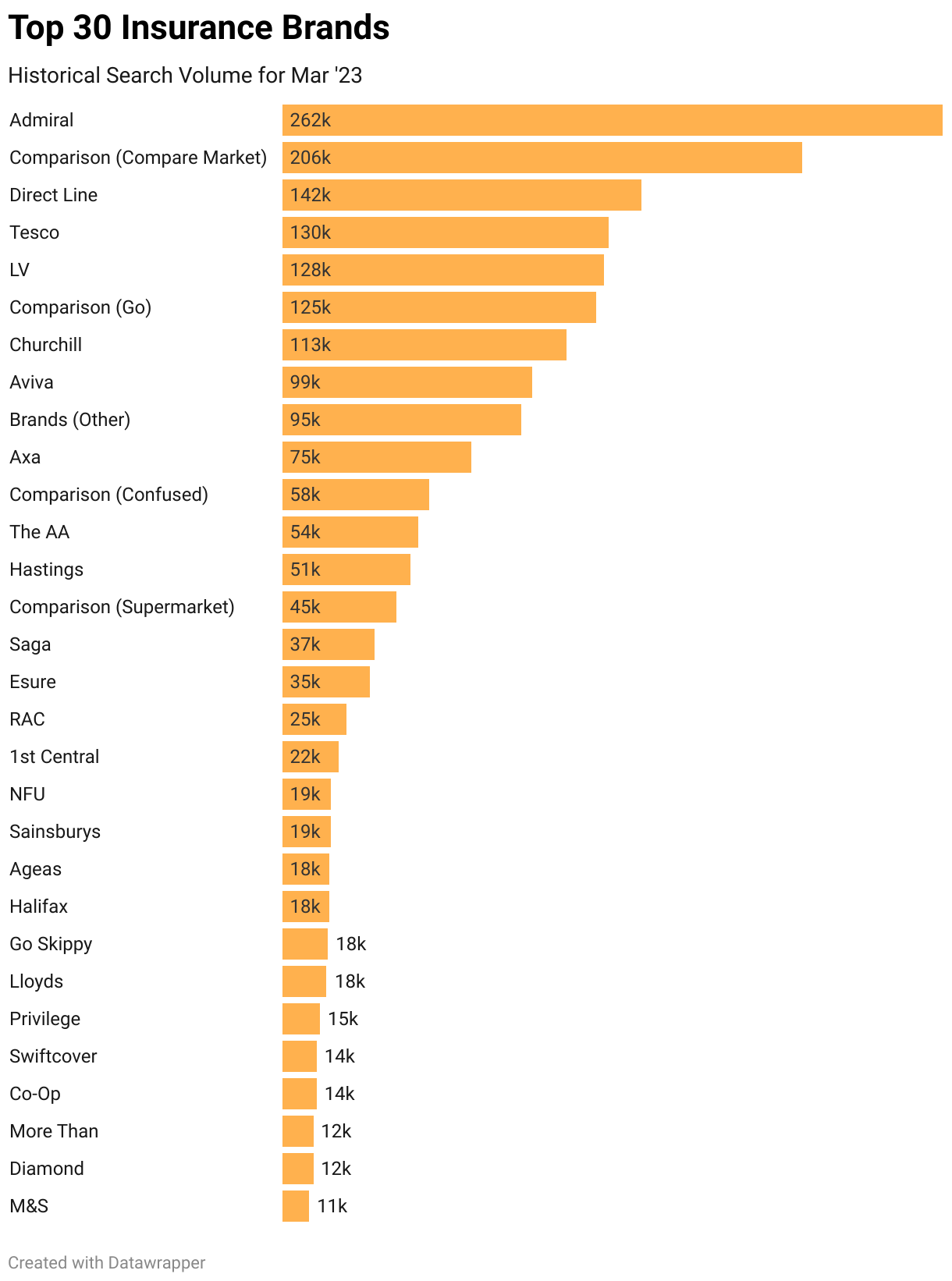

What are the most popular brand searches when it comes to Car Insurance?

A lot of household names in this list well known from TV advertising campaigns but even so, its a surprise to see Admiral topping the list even above the comparison sites (go compare, compare the market, confused, etc)

Brand demand does fluctuate widely based on the TV advertising schedule of when ads are being aired month by month so the landscape is always changing.

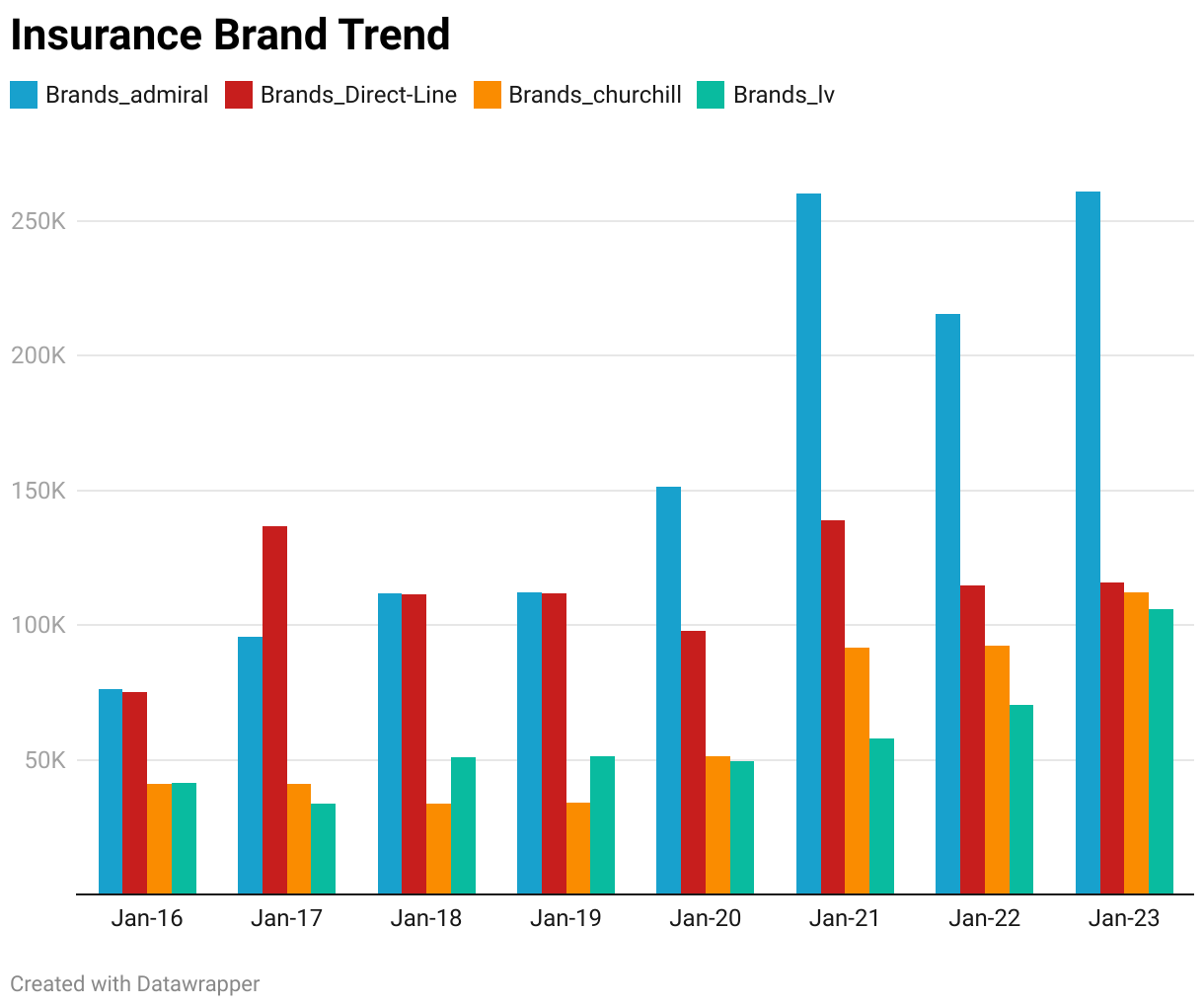

“Selected” Insurance Brand Trends

Admiral’s brand awareness did not skyrocket until somewhere during 2020 but I have no explanation as to why or how!

Direct Line used to be neck and neck with Admiral but they have not kept pace and in fact, most recently, LV and Churchill have closed the gap on them

Churchill and LV brand awareness is comparable and they’ve recently joined Direct Line in the “chasing pack” behind Admiral

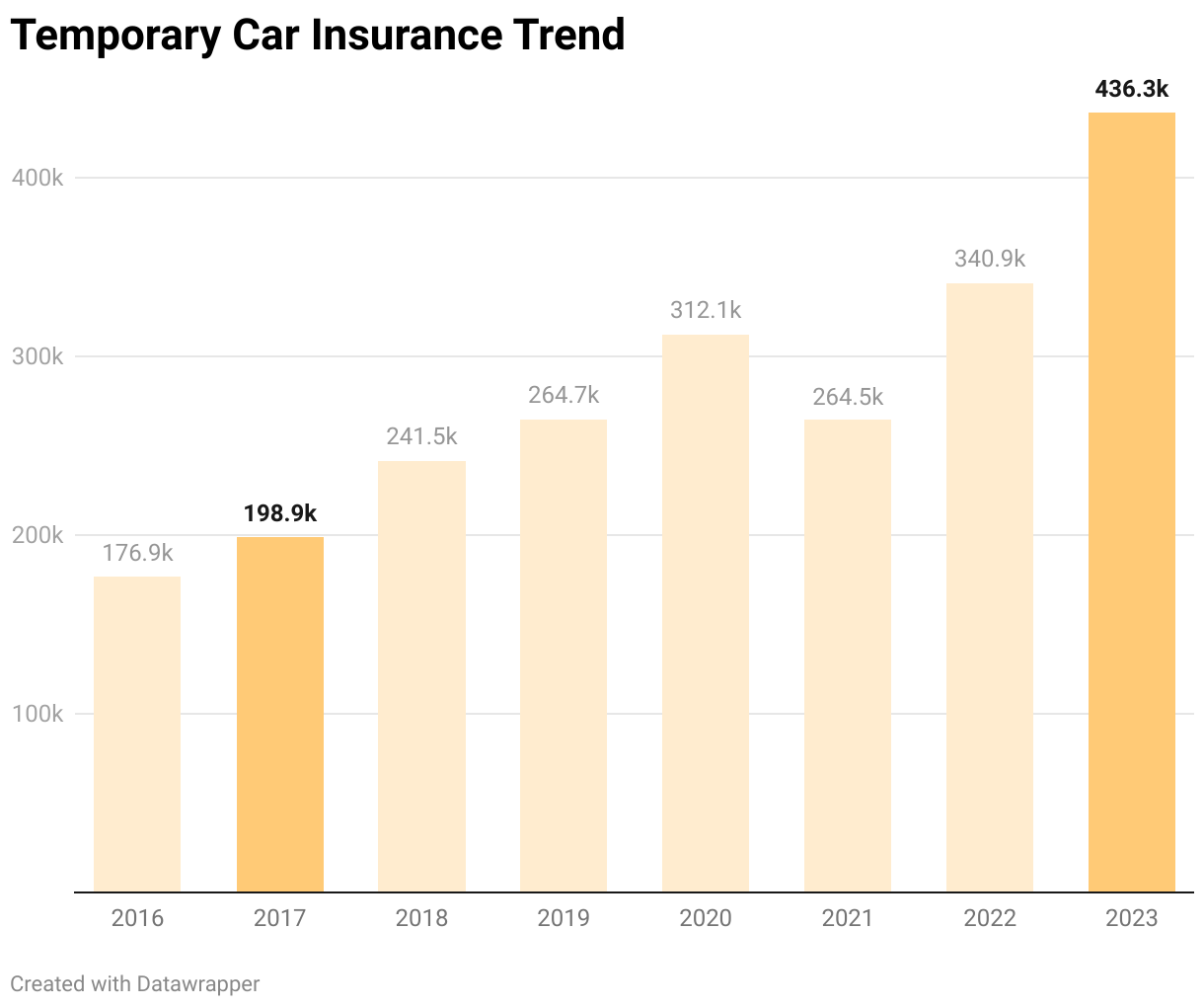

“Temporal” Car Insurance

It feels like there is a lot of work being done within the industry to deliver this as a new breakthrough category. Since 2017 these terms have doubled but from a pretty low base.

Jan 2023 total market size was 3.9M and with 430k searches for “temp” terms this is roughly 10 - 15% of the total market.

So it’s not a game-changer.

In Summary

That’s a lot of useful information waiting to be explored!

Would be beneficial for:

Digital “Due Diligence” for Venture Capital firms

Business Case analysis for Start-Up funding to quantify size of opportunity and the media spends required

Independent analysis for current in-market businesses looking to benchmark themselves, (re)discover industry specific insights and the latest trends

Business opportunities for matched market testing in new markets or expansion into new product spaces

Get in touch to find out about a specific area of interest, industry or vertical by country, continent or language.

Methodolgy of Data Set

It is important to understand and make valid assumptions to provide more confidence in the answer, especially if it’s being used to make a business decision.

Some of the considerations that were made about this data to increase confidence in the answers:

Match Type Assumptions

regardless of the market, never use broad match when looking for a specific answer as all control on the keyword data set is lost

Exact Match will always provide accurate data for the keyword data set but perhaps the keywords chosen do not adequately reflect the whole of the market that is available. It is favourable in many other ways however as e.g.

historical trend data can only contain exact match terms

it eliminates the need for “negative” terms that are necessary when forecasting with phrase match.

Phrase match is a safe bet as the keyword research has been carried out to add breadth while excluding non relevant terms with the aim that the data set is wide enough while intelligently removing “low intent” and “no intent” search terms.

Beyond market size there is also a consideration of budget required to capture the market share based on a forecast model for which “phrase match” will always provide a fuller picture as it will reach more searches and have reduced costs per click compared to exact match.

Historical Data

Historical trends in Google Keyword Planner uses exact match keywords. Language settings are also ignored while Network settings can still be chosen as desired. As a result of these limitations, the use of trends and forecasts of consumer behaviour should be carried out as a distinct exercise from estimating market size that focuses more on the general trends rather than the absolute numbers.

New assumptions for historical trends and forecast settings are:

Use Exact Match keywords only (only option for historical trends)

Include all languages (only option for historical trends)

Use Google only (this will reduce total forecast market volume) but increase accuracy and focus on valid user searches on Google only

For this reason and many others it is essential that a reasonable amount of keyword research has been carried out and nuances of the market place are adequately accounted for as market research based on:

a handful of exact match keywords is a poor approximation

phrase match forecasts will not align with historical (exact match only) data from the Keyword Planner tool

Forecasting Data

To seamlessly combine looking back at historical trends with looking forward to monthly forecasts and predictions requires a tweak of the previous assumptions for generating a picture of the general landscape and average market size of the car insurance market. The process to approximate the actual market size goes something like this:

Generate and establish a robust data set (a large enough set of keywords and negative keywords)

Find a mid-point based on some assumptions. In this case it was “Lets use phrase match and Google only”

Add some colour with bid estimates to establish a range of budgets that approximates competitiveness and cost